Table of Contents

What Are Contract Bonds?

A contract bond is a legally binding agreement that guarantees a contractor will fulfill the terms of a construction or service contract. These surety bonds protect project owners (obligees) by ensuring the contractor (the principal) completes the work as promised. A third party, known as the surety, backs this promise and steps in if the contractor defaults on their obligations.

Construction bonds are the most common form of contract bond on construction projects. They are widely required in public works projects and are also frequently mandated in private construction. By securing a bond, both local contractors and national firms demonstrate financial stability, reliability, and a commitment to fulfilling project obligations.

The terms “contract bond” and “construction bond” are often used as synonyms.

How Does a Contract Bond Work?

Each contract or construction bond involves three parties:

- Principal – the contractor responsible for the work.

- Obligee – the project owner requiring the bond.

- Surety – the bonding company guaranteeing the obligations.

If the contractor defaults, the obligee may file a claim. When valid, the surety compensates the obligee for financial losses, then seeks repayment from the contractor. Unlike insurance, where the risk is pooled, surety bonds place ultimate responsibility back on the contractor.

This structure is critical in construction, where owners, general contractors, and construction subcontractors depend on timely completion and payment.

When Do You Need a Contract Bond?

Contract bonds are required on many construction projects to protect owners and ensure performance and payment to subs and suppliers. Here’s how it breaks down by project type:

Federal construction projects (U.S. government)

- When required: On most federal construction contracts over $150,000 (Miller Act). For $35,000–$150,000, agencies require payment protection (often a payment bond or approved alternative).

- Common bonds: Bid bond (when solicited), Performance bond (100% of contract), Payment bond (100%).

- Who must issue the bond: A Treasury-listed surety acceptable to the U.S. government.

- What the contractor should expect to provide: Company and personal financials, work history, current work-in-progress (WIP), and indemnity.

- Small business help: Many small or local contractors qualify via the SBA Surety Bond Guarantee program when a traditional surety bond for contractors is hard to place.

State & local public works (“Little Miller Act” projects)

- When required: For public construction let by states, counties, cities, school districts, etc. Thresholds and percentages vary by state (some require bonds above $25k, others at higher amounts).

- Common bonds: Bid bond (amount set by statute or the solicitation), Performance & Payment bonds (often 100%, but state statutes or bid docs control).

- Who must issue the bond: A surety licensed in the state (some owners specify minimum A.M. Best ratings).

- What to watch: State-specific bond forms, notarization/seal language, attorney-in-fact authority, and notice/claim deadlines for suppliers and subs.

Private/commercial construction & development

- When required: Not mandated by law; owners, developers, or lenders require bonds to manage risk - common on larger vertical builds, tenant improvements, and financed projects.

- Common bonds: Bid, Performance & Payment, plus Supply/Material bonds when procurement risk is high.

- Development/site work: Municipalities often require subdivision/improvement bonds (to guarantee streets, utilities, and sidewalks) before plat approval or issuance of permits.

- Who sets the rules: The contract and loan documents - look for dual-obligee or lender rider language, surety rating minimums, and consent-of-surety requirements.

- What the contractor should expect to provide: The same surety underwriting package (financials, WIP, experience, indemnity) and, at times, additional owner/lender qualification forms.

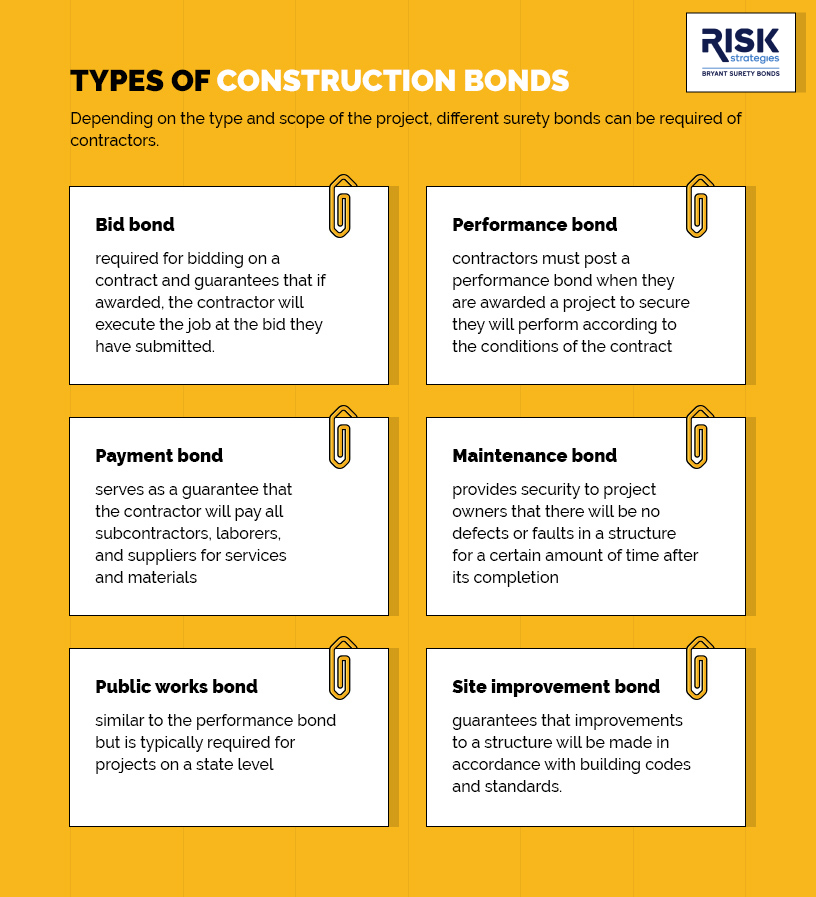

Types of Contract Bonds

There are several types of contract bonds, but the three primary ones are bid bonds, performance bonds, and payment bonds. Each is designed to cover a different aspect of a project. In most construction contracts, more than one type may be required.

- Bid Bonds – Ensure a contractor will honor their bid and sign the construction contract if awarded.

- Performance Bonds – Guarantee completion of the project according to contract terms.

- Payment Bonds – Protect construction subcontractors, suppliers, and laborers by ensuring they get paid.

- Subdivision Bonds – Required by municipalities to ensure infrastructure improvements such as roads, sidewalks, and utilities.

- Site Improvement Bonds – Guarantee upgrades or modifications to existing properties.

- Contractor License Bonds – While technically license and permit bonds, they are often grouped with contract bonds for contractors needing licensing compliance.

- Public Works Bonds – Bonds required on state/local government projects, usually statutory performance and payment bonds guaranteeing completion and payment per the bid specs.

- Maintenance Bonds – Post-completion warranty bond (often 12–24 months) that covers defects in workmanship/materials; typically 5–20% of the contract amount.

Together, these bonds provide a full safety net for owners, subcontractors, and project stakeholders.

How Much Does a Contract Bond Cost?

The actual construction bond cost that you will pay is called a bond premium, typically ranging from 1% to 3% of the bond amount for qualified applicants. For example, a $100,000 bond usually costs between $1,000 and $3,000.

Your exact construction bond rate depends on:

- Personal and business credit history

- Financial strength, such as tax returns and balance sheets

- Contract size and bond amount

- Past project experience and performance record

- Current workload and bonding capacity

- Geographic and project-specific risks

Contractors with strong credit, solid financials, and a proven track record generally qualify for the lowest rates. Those with less-than-perfect credit may still obtain a bond, but at higher premiums, since the surety assumes greater risk.

-

1Get a FREE Bond QuoteStart Your Application

-

2Tell us about your businesspowered by

-

3Get your FREE quote today!

How to Get a Contract Bond

The process to get a surety bond for contractors is straightforward, though the steps vary by project size.

- Tell us about your project: Complete the quick form with your business and project details.

- Get your rate & approval: We review your info and present your best available quote - often in minutes.

- Pay & receive your bond: Pay online and instantly download or have the bond sent to your obligee.

For small construction projects, bonds can often be issued within a day. Larger jobs may take several days as underwriters review financials and bonding capacity.

FAQs

Are contract bonds the same as construction bonds?

Yes. On construction projects, a contract bond package typically includes bid, performance, and payment bonds.

Do I need a bond for every project?

Not always - public work often requires it, while private construction contracts depend on owner/lender risk requirements.

How much bonding capacity do I need?

Capacity reflects the total bonded work you can handle at once; it grows with experience, financials, and proven bonding performance.

What is the difference between contract bonds and payment bonds?

A contract bond is the overall package; a payment bond specifically guarantees payment to construction subcontractors and suppliers.

How long does it take to get bonded?

Small bonds can be issued the same day. Larger or more complex projects may require additional time.

Do contract bonds expire?

Most are tied to one job and remain active until the construction contract is fulfilled; maintenance bonds extend into the post-completion period.

Frequently Asked Questions

Still Have Questions?

Still haven't found the answer you are looking for?

Give us a call at 866.450.3412 or leave your question below.