Table of Contents

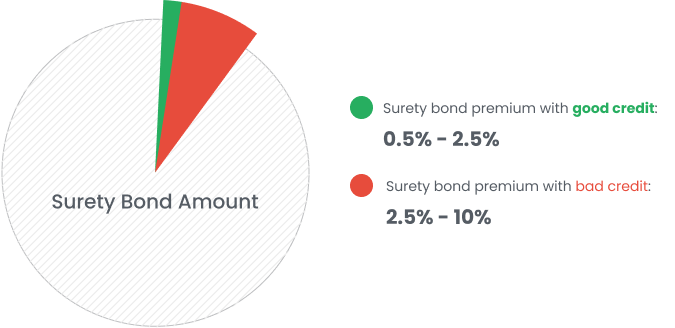

The surety bond cost usually ranges between 0.5% to 10% of the bond amount. Several factors determine the price, including the type of bond and bond amount, the associated risk, and the applicant's qualities.

How Is the Bond Cost Calculated?

To understand how the cost of a surety bond is determined, you must understand the bonding process, how surety bonds work, and the parties involved. Surety bonds are legally binding agreements between the principal, the obligee, and the surety.

The bonding process starts when a business is required to secure a surety bond, often from a government agency or private party. Once the principal has determined the type of bond needed and the state requirements, a surety company will work with the business to apply for the required bond, requiring the submission of various documents to evaluate the business's risk.

The surety company then undertakes an underwriting process to evaluate the risk associated with issuing the bond. Once approved, the bond company will provide a surety bond rate quote, determining the premium. The surety bond price can be increased for a partial-year term or decreased for a multi-year bond term. Additionally, some surety companies offer discounts for purchasing bonds with multiple one-year terms.

The surety bond cost reflects the risk assessed during underwriting, which considers factors such as the applicant’s credit history, financial stability, experience, and past project performance. Higher perceived risk results in higher premiums, with rates ranging from as low as 0.5% to over 10% of the bond amount, depending on the applicant's risk profile.

Surety companies act as guarantors, promising to cover a financial obligation if the principal fails to meet the required conditions. By thoroughly evaluating these elements, sureties aim to predict the likelihood of a claim and adjust the bond premium accordingly to compensate for potential risks.

Understanding these factors is crucial for grasping how bond costs and approval are determined.

Key Factors Affecting Bond Costs

Some of the most important factors surety underwriters might consider when determining which rate category the surety bond you are seeking falls into are discussed below.

Surety Bond Amount

The bond amount is directly related to the bond’s purpose and the associated risks involved. The surety bond cost is calculated as a percentage of this total bond amount, meaning that higher bond amounts generally lead to higher premiums.

The bond amount represents the maximum coverage the surety will provide in the event of a claim, so the riskier the bond's purpose, the larger the bond amount typically required, and consequently, the higher the premium. The cost is a percentage of the bond amount. For example, a $100,000 bond at a 1% rate costs $1,000, while a $1,000,000 bond at the same rate costs $10,000.

Surety Bond Type

The surety bond type significantly impacts the premium due to the varying levels of risk associated with different industries and purposes. Applicants considered to be in lower-risk categories tend to receive lower premiums. The industry and the specific purpose for which the bond is required directly influence the perceived risk and thus affect both the bond amount and the premium. Typically, you can expect to be charged a higher rate for a payment bond or a tax bond than those that guarantee compliance with permit or license requirements.

For instance, in the freight broker industry, the prevalence of fraud has led some surety companies to either avoid writing these bonds or to charge substantially higher rates compared to bonds in other industries.

Credit Score

Your credit score is one of the most critical factors that surety bond providers consider when determining your bond premium. A higher credit score generally indicates financial reliability and responsibility, which typically results in lower bond premiums. Since your credit score reflects your creditworthiness and financial history, it is a key indicator for sureties in assessing the likelihood of future claims.

The table below shows examples of surety bond rates for some of the most popular surety bond types.

| Surety Bond Amount | Applicant's Credit Score | |||

|---|---|---|---|---|

| Excellent Credit Score (650 and above) | Average Credit Score (550-649) | Below Average Credit Score (549 and under) | ||

| $5,000 Surety Bond | $100 | $100-$375 | $375-$500 | |

| $10,000 Surety Bond | $100-$250 | $250-$750 | $750-$1,000 | |

| $15,000 Surety Bond | $112.5-$450 | $450-$1,125 | $1,125-$1,500 | |

| $25,000 Surety Bond | $188-$750 | $750-$1,875 | $1,875-$2,500 | |

| $30,000 Surety Bond | $225-$900 | $900-$2,250 | $2,250-$3,000 | |

| $35,000 Surety Bond | $262-$1,050 | $1,050-$2,625 | $2,625-$3,500 | |

| $50,000 Surety Bond | $375-$1,500 | $1,500-$3,750 | $3,750-$5,000 | |

| $75,000 Surety Bond | $563-$2,250 | $2,250-$5,625 | $5,625-$7,500 | |

| $100,000 Surety Bond | $750-$3,000 | $3,000-$7,500 | $7,500-$10,000 | |

| $500,000 Surety Bond | $3,750-$15,000 | $15,000-$37,500 | $37,500-$50,000 | |

| $1,000,000 Surety Bond | $10,000-$20,000 | $20,000-$40,000 | $40,000-$50,000 | |

Assets

Ownership of significant assets indicates a lower financial risk because it shows that you have resources available to cover potential claims if they arise. Having sufficient assets can reassure the surety that you are financially stable, potentially leading to a lower premium.

Financials

Both business and personal financials play a crucial role in determining your bond premium. Positive financial statements indicate that you are financially capable of fulfilling your bonding obligations. A financially stable business means there is a lower chance you will not follow through with your bonding obligations, which can lead to a more favorable bond quote. Personal financials, such as ownership of assets, further reduce the perceived financial risk in case of a claim.

Industry Experience

Businesses with experience are considered more reliable. Sureties are more likely to offer lower rates to individuals and businesses with a proven track record of completing projects and meeting obligations. On the other hand, those with less experience may face higher premiums due to the increased perceived risk associated with their lack of a proven history.

Previous Claims

A history of previous surety bond claims can significantly impact your bond cost and approval chances, often leading to higher premiums or even rejection. For example, if a construction contractor has had multiple claims filed against their performance bond in the past, future surety providers may view them as a high-risk applicant. As a result, the contractor might face much higher premiums when applying for new bonds, or they could be denied coverage altogether.

Surety Provider

Selecting the right surety provider is crucial, as different companies have varying levels of risk tolerance. It's a good idea to compare quotes from multiple sureties, as each evaluates risk differently. For example, at Bryant Surety Bonds, we work with a surety bond company that offers lower freight broker bond quotes due to their extensive industry experience and high bond issuance volume. Therefore, we try to bond most of our freight broker applicants through this surety. The same goes for other industries and surety bond providers. We work with the top-rated surety bond companies in the US to provide the lowest possible bond rates to all applicants.

Estimate your surety bond premium with our free surety bond cost calculator.

Surety Bond Cost Calculator

Tell us where to send you your FREE estimate

SEND ME MY ESTIMATE!We'll never share your information with third parties

Thank you for your request!

The ballpark estimate on your premium is: $100 - $167

We've sent a copy of your estimate on your email as well.

Want an exact quote? Simply fill out our online application It's fast and 100% free!

Get a free exact quote Get another estimateWhat Is a Surety Bond Amount?

The Surety Bond Amount also known as the bond limit is the maximum amount of liability coverage provided by the bond.

The maximum surety bond amount is not the same as your bond cost. For example, if you are required to secure a $50,000 surety bond, you will not have to pay $50,000 upfront to secure the bond. Instead, the maximum bond amount equals your liability and is the bond's penal sum. The premium you will pay for the bond will be a percentage of the total amount. However, if a claim is filed against your bond and you fail to pay it, you can be held liable for up to the maximum amount of your bond.

Surety Bond Rates

Your surety bond rate is the percentage of the total bond amount you must pay to get bonded. This rate is determined by the surety based on an assessment of your business, financial strength, and the type of bond required. The rate, influenced by the above-mentioned factors like your credit score and overall finances, directly determines your bond's cost.

Surety Bond Costs by Bond Type

The costs of different surety bonds by bond type are discussed below.

License & Permit Bonds Cost

License bonds are required by state and local authorities for certain industries to provide financial protection against fraudulent practices and non-compliance with local regulations. The cost of a license bond depends on the bond amount and credit score. High scores result in lower costs. The final surety bond price is determined by the bond company reviewing the application.

The freight broker industry is a specific example of residual risk after a thorough evaluation of the factors. Due to increased fraud in recent years, some sureties have stopped issuing these bonds altogether. In case you need a freight broker license, you would also need to obtain a freight broker bond. The cost of a freight broker bond typically ranges from 1.25% to 5% of the $75,000 bond amount, or approximately $938 to $11,250 annually, depending on factors including the credit score, financial strength, and industry experience.

To illustrate how credit scores impact bond costs, below is a breakdown of example rates for different types of license bonds based on credit score.

Example Rates By Surety Bond Type

| Credit Score/ Type of Bond | Auto dealer bond | Freight broker bond | Mortgage broker bond | Tax & utility bond | Other license bonds (avg. rate) |

| 700+ | 0.75%-1.5% | 1.25%-3% | 0.5%-1.25% | 1%-3% | 0.75%-1.5% |

| 650-699 | 1%-3% | 3.5%-5% | 0.75%-1.5% | 2%-5% | 1%-2.5% |

| 600-649 | 2.5%-5% | 7.5%-10% | 2%-5% | 15%-17% | 2.5%-5% |

| 550-599 | 5%-7.5% | 10%-12% | 5%-7.5% | 15%-17% | 5%-7.5% |

| 549 and under | 7.5%-10% | 12%-13% | 5%-10% | 15%-17% | 5%-10% |

Contract Bonds Cost

Contract bonds are contractual obligations for construction projects, requiring contractors to file bid bonds and final bonds with the project owner. The surety company is an insurance carrier licensed to operate in the state where the project is handled. Contract bonds protect the owner against failure to complete a project and nonpayment for materials and labor.

The cost of a contract bond varies between 1% and 3% of the total contract amount, depending on factors like project size and contractor reputation.

Fast Track Contract Bonds

Several surety markets will write credit-based contract bonds. Typically, this type of app is used when the job is $500,000 or less, you (the contractor) have no or limited bonded experience, and your credit is strong (read 650+ clean). A contractor using a credit-based program can expect a premium that is 3% of the bond amount required. While a few markets will consider those with lesser credit, the majority do not.

Full Bond Line Projects

For experienced contractors that need a full bond line (larger jobs, or contractors that are doing several jobs at once), a more thorough underwriting process will take place. Financials (2-3 years of CPA-prepared, reviewed financial statements (not tax returns), on an accrual, cost-of-completion basis with full notes and disclosures), Work on Hand schedule, bank reference letter, and more will be reviewed. Full bond lines are quoted on a sliding scale, so the larger the job, the smaller the bond rate will be.

Fidelity Bonds Cost

A fidelity bond is a surety bond obtained by businesses handling other people's property or finances. It works like insurance, protecting a business from damages due to employee dishonesty, theft, or embezzlement. There are three main types: business service bond, employee dishonesty bond, and ERISA bond. Business services bonds protect employees' property, while employee dishonesty bonds protect financial institutions. ERISA bonds protect pension and employee benefits plans from fraudulent managers.

Costs depend on the business type, coverage amount, and number of employees. One example of a fidelity bond is the ERISA bond, required of every person who handles employee retirement plans. The cost of an ERISA bond typically ranges from 0.75% to 2.5% of the bond amount, depending on the applicant’s credit score and financial indicators.

Court Bonds Cost

Court bonds are surety bonds required in court proceedings to protect obligees from financial loss. Common scenarios include the appeal of a court's judgment or the appointment of a fiduciary by a probate court. Court bonds are made between the obligee, principal, and the surety bond company. Different types of bonds include supersedeas bonds, fiduciary bonds, guardianship bonds, injunction bonds, replevin bonds, VA fiduciary surety bonds, and bankruptcy trustee bonds.

The cost of court bonds depends on the specific case and bond, with appeal bonds requiring 100% collateral and fiduciary bonds requiring a premium. For example, for a fiduciary bond, the premium is between 1% and 3% of the bond amount. If we take an estate costing $100,000, your bond premium will range between $1000-$3000. Larger bonds often have premiums below 1% due to a sliding scale.

Surety Bond Cost-Saving Tips

To help make your bond premium as affordable as possible, you can follow these easy tips:

-

Make Sure Your Credit Score is accurate: Fixing any errors can help improve your credit score and lower your bond rates.

-

Improve Your Personal Credit: Manage your debts well. Make a budget, pay bills on time, avoid new credit applications, and settle old debts to boost your credit score.

-

List All of Your Assets: Presenting the surety bond agency with information about your capital, collateral, licensure, and business structure will help lower your premium. Having assets will demonstrate your ability to run a stable business. Don’t forget to indicate all assets in your financial statements.

-

Get US Citizenship: Many surety companies offer better rates to U.S. citizens. If you're not already a citizen, consider the process to gain citizenship and potentially lower your bond rate.

-

Show Strong Financial Statements: For larger bonds, show that your business is financially healthy. Provide accurate reports of your assets, income, and cash flow.

-

Buy a Long-Term Bond: Some companies give discounts if you buy a bond for multiple years instead of just one. This can save you money over time.

-

Add a Cosigner: If your credit isn’t great, find someone with good credit to cosign your bond. This can lower your rate because the company will consider both credit scores.

-

Use a Payment Plan: Spread out your bond payments over several months to make them more manageable. This can help with your business’s cash flow.

-

Choose the Right Surety Agency: Look for an agency like Bryant Surety Bonds that offers great premium rates and does not have any additional hidden fees.

FAQ

Can I get bonded with bad credit?

You can obtain a surety bond even if you have bad credit, a low personal credit score, or past bond claims. High-risk applicants or new businesses with bad or minimal credit history will pay higher surety bond premiums. New companies with unstable cash flows and past credit issues are also considered higher risk. Surety companies use varying premium rates based on credit scores, but approval is possible as long as you can pay the initial premium. To determine the rate that you might have to pay, use a bond cost calculator and check our Bad Credit Program.

Which companies provide cheap surety bonds?

Bryant Surety Bonds is among the companies that provide affordable surety bonds, and it is known for its competitive rates and quick approval. The cost varies based on the different factors mentioned in the article. Bryant Surety Bonds will help you get the best quote possible using their industry experience and connections.

Are surety bonds paid monthly?

No, surety bonds are paid on an annual basis.

What is the average cost of a bond?

The surety bond cost varies between 0.5-10% of the bond amount. For example, a bond with a coverage amount of $50,000 might cost anywhere from $250 to $5,000.

Start your online application and receive a free surety bond quote in minutes.

What is a surety limit?

The surety limit is the maximum amount the bond company will pay if the principal fails to fulfill their obligations.

Frequently Asked Questions

Still Have Questions?

Still haven't found the answer you are looking for?

Give us a call at 866.450.3412 or leave your question below.